It’s about Loss of Face! Writing off bad debts to banks causes loss of face to both the Banks and the Borrowers.

Read moreSome years ago I discovered that the tax-driven investors in Timbercorp had stumbled into a ponzi scheme. Normally I can unravel these schemes quickly — but this one took me three days!

Read moreAmerica's RICO (Racketeer Influenced and Corrupt Organisations) Act has allowed lawmakers to bust open many criminal and corporate criminal enterprises that were otherwise too hard to convict. Australia desperately needs similar laws.

Read moreWould an actuary tell a lie? Or a fib? Or make a 'misrepresentation'? This article says 'yes' — at least to the fib level — and reveals a very tricky bit of number crunching that actuaries use to make themselves look smart.

Read moreMany people will love these ideas. Many will hate them. Most people will like the ideas that help their hip pocket and/or their children’s future.

Read moreXi Jinping is without question the most powerful leader of China since Mao Tse-Tung

Read moreAre Australia’s big 4 Banks Caught between the Rock of Basel III and a Hard Place of their own making?

Read moreAustralian Banks' profits and dividends are going to be under downward pressure as they face a perfect storm of negatives.

Read moreIn this lecture Peter gives an overview of investment markets and decision making frameworks.

Read moreDonald Trump's mastery of Twitter helped him to win the white House - but a lack of trust in Hilary Clinton played an even greater role.

Read moreMany medical specialist earn (after costs but pre-tax) in excess of $1 million per annum.

The main solution would be for the federal government to fund many more registrar positions in state government hospitals. This would generate more skilled specialists, and competition would drive their prices down.

Read moreWhile Australia has one of the best and more cost effective health systems in the Western world, it suffers from a major anomaly. The Federal Government pays (via the Medicare Levy and other taxes) all of the standard costs of Medical Procedures and General Practitioner Costs. The State Governments pay for the costs of running and staffing Public Hospitals.

Read moreTwitter is an online news and social networking service where users post and interact with messages, "tweets," restricted to 140 characters.

Read moreIn just over 40 years of experience in the corporate world, I have seen, or heard of just about everything that Boards, Chairman, and Company Secretaries can get wrong.

Read moreMany people will love these ideas. Many will hate them. Most people will like the ideas that help their hip pocket and/or their children’s future.

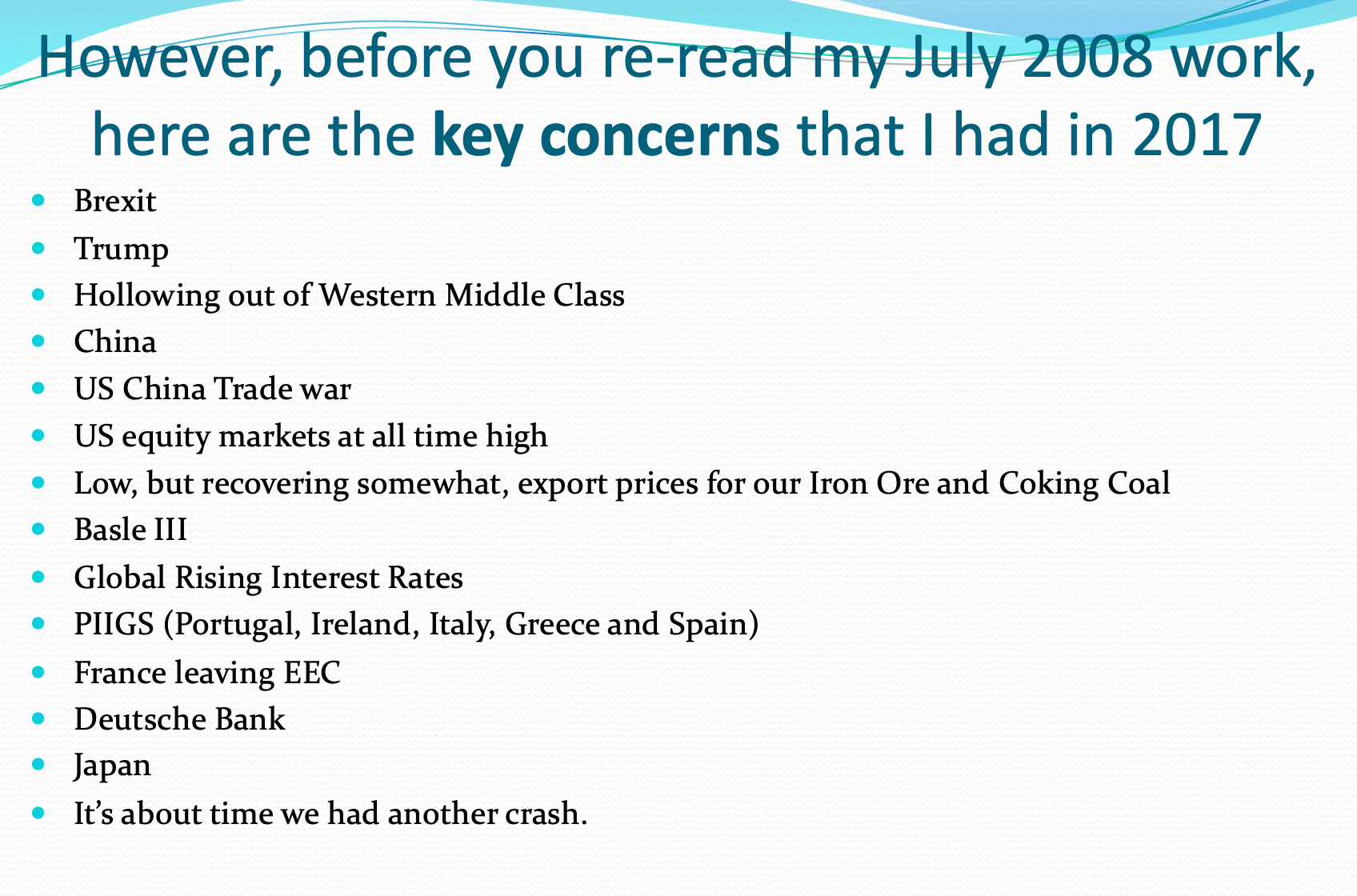

Read more2017 is already shaping up as the most dangerous year since 2008 for financial markets - but for completely different reasons.

Read moreThis “golden” number, 1.61803399, represented by the Greek letter Phi, is known as the Golden Ratio, Golden Number, Golden Proportion, Golden Mean, Golden Section, Divine Proportion and Divine Section. It occurs everywhere in the world around us.

Read moreWhen university is over your real education begins!

Read moreThose who do not learn from history are doomed to repeat it.

Read more